The Quick Commerce Rocket Changes Trajectory

Boosters jettisoned, Stage 2 initiated

Over the last year-and-a-half, I made 2 predictions on when Quick Commerce growth in India would start to moderate.

The first one was off by 6 months. The second one looks like it’ll stick the landing.

Order Placed

The First Prediction

In Dec’24, Praveen Gopal Krishnan, COO at The Ken, asked readers of his Nutgraf newsletter to share their predictions for 2025. I sent in mine, and he was kind enough to include it in the next edition.

While you can see my detailed rationale here, this was the gist of my prediction:

“By mid-2025, I expect to see quick-commerce MTUs plateau, as these players hit their natural limits on users and cities (given that neither offline nor online consumers are showing strong underlying consumption growth trends at present)”

(MTUs are Monthly Transacting Users)

Order Delayed - Awaiting Rider Assignment

Reality Takes A Different Path

It soon became clear that I had considerably underestimated the latent demand for quick commerce (henceforth also referred to as QC). When I made that prediction, Blinkit was at 9M MTUs, and eGrocery as a whole (including slotted, quick and other delivery models) was at 25M MTUs.

Today, Blinkit alone has 27M MTUs, while quick commerce has over 50M MTUs, per Redseer.

The rationale behind my prediction was twofold:

Quick commerce growth was being driven by channel shifts from GT and MT, which would likely peter out over time (while overall private consumption had already started slowing from H2 2023 onwards)

Total eGrocery MTUs at that point would likely be a ceiling for quick commerce MTUs, given that eGrocery had been fairly well-established by BigBasket, with a post-Covid jump in adoption

On point 2, in hindsight, eGrocery MTUs weren’t the right benchmark to use. Online Food Delivery (OFD) MTUs may be a more appropriate benchmark here (it’s a short jump from having prepared food delivered to having groceries delivered, for affluent customers who value convenience).

And interestingly, for Eternal and Swiggy, the ratio of combined QC MTUs to combined OFD MTUs (including overlaps), which was 65% in Mar’25, has grown to 93% in Mar’26.

I’m not calling it a ceiling, given that grocery is a much larger market than restaurant food - but it’s an interesting frame of reference.

On point 1, though; the broader trend of QC growing more through channel shifts from GT and MT than by generating new consumption seems fairly well-established now, and continues as we speak (or read, in this case).

Order Dispatched, Tap To Track Rider

The Second Prediction

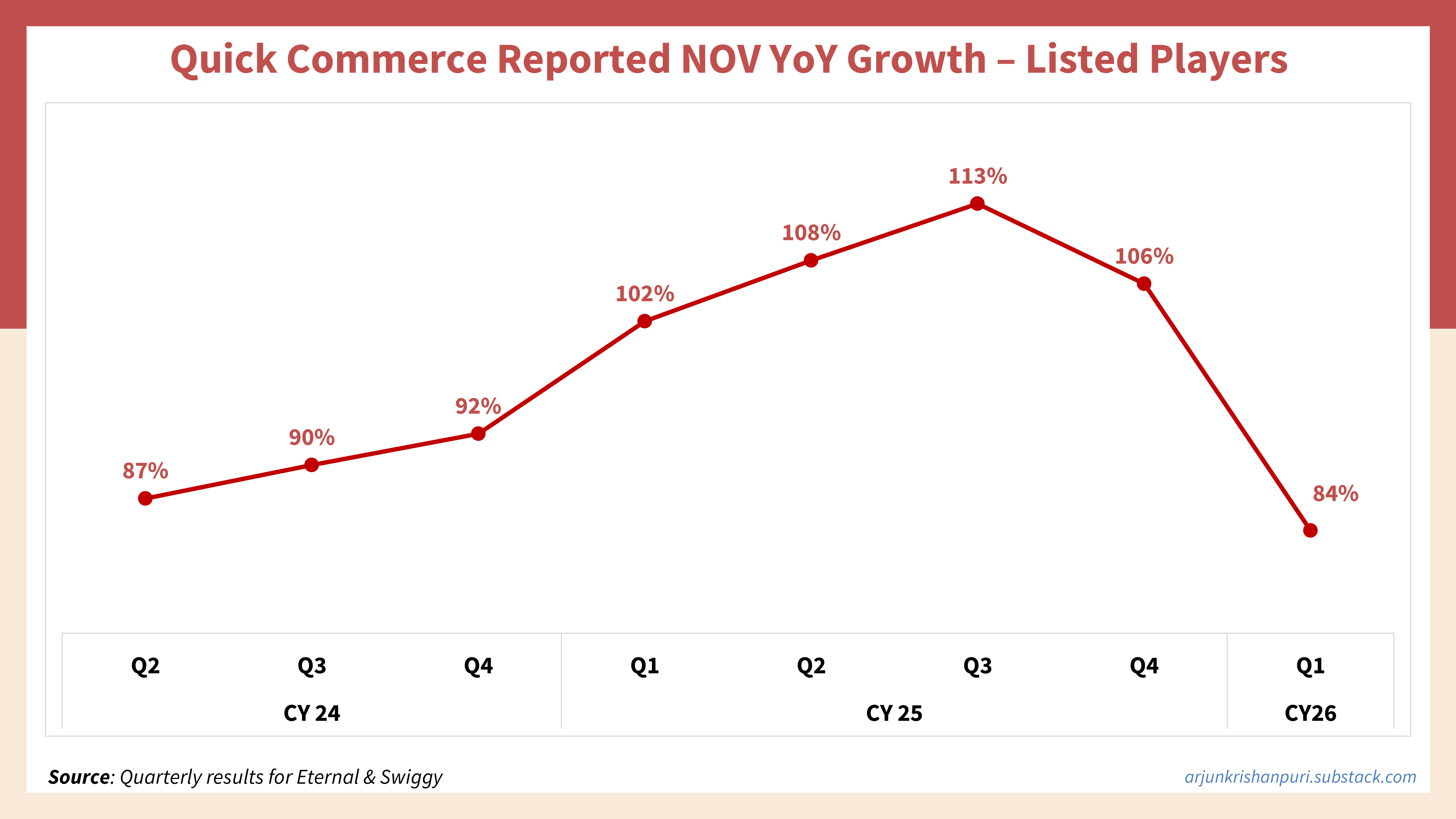

Quick commerce grew at a scorching pace in 2025, boosted by a surge in dark store additions in Q4’24 and Q1’25 which drove GOV (Gross Order Value) / NOV (Net Order Value, after discounts) growth of over 100% for Blinkit and Instamart. Through all of that year, it seemed like the quick commerce rocketship would continue to defy gravity over the near to medium term.

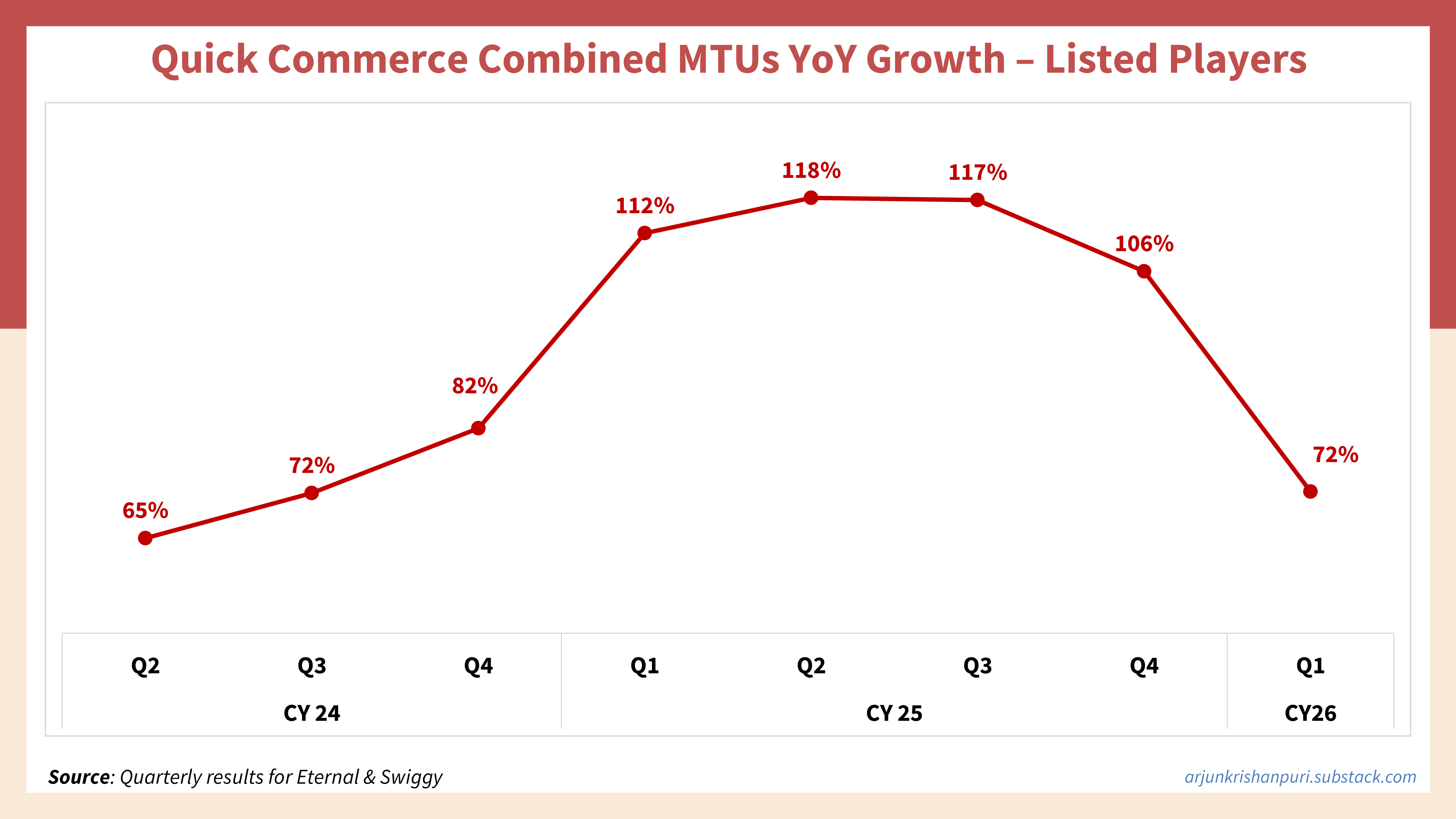

However, when Q4’25 results were released, in Jan’26, I noticed something curious - YoY growth in combined Blinkit and Swiggy MTUs was at a four-quarter low. Across the four quarters of CY 2025, this growth was 112%, 118%, 117% (mathematically lower, but could easily have been a blip)… and 106%.

Of course, 106% is an absurdly high MTU growth rate - but it did suggest a softening of momentum.

As I’d written on LinkedIn at that time, reported NOV growth for Q4’25, which was also 106%, was lower than the previous quarter’s growth for the first time after 5 quarters of increasing growth rates. However, both Blinkit and Instamart highlighted that NOV growth for that quarter was impacted by the cut in GST rates (leading to lower selling prices) and some festivals shifting to Q3 in 2025 (vs Q4 in 2024). After adjusting for these factors, NOV growth for Q4’25 could plausibly have been higher than in Q3’25… So NOV growth wasn’t a clean trend to go by.

However, based on the MTU growth trajectory, I went ahead and published my second prediction:

“Given this data point - I'm going to stick my neck out and say that we might be at (or very close to) peak growth rates for Quick Commerce.”

Order Delivered

A Visible Shift In Momentum

…Which brings us to where we stand today.

Over the last five weeks, Blinkit and Instamart declared their results for Q1’26. And what could potentially have been a blip in Q4’25, is now a clear change in trajectory - growth in combined NOV as well as MTUs is now gently sloping downwards.

Both metrics are still growing rapidly, but we do indeed seem to be past peak Quick Commerce growth.

Note: In its Q1’26 shareholder letter and analyst call, Swiggy did highlight that from Jan’26 onwards, they’ve taken a conscious decision to churn out low-AOV (Average Order Value) shoppers, which impacted their MTU growth and likely led to a sharper-than-expected fall in this MTU growth chart. But that being said, I’m reasonably confident that the shape of this chart would have been the same even if they hadn’t made this choice.

Both platforms have also shared guidance indicating that GOV / NOV growth over the next few years will moderate to 60%+ (Blinkit) and 35-50% (Instamart), down from the 100%+ levels seen in 2025, which further supports our hypothesis.

Unpacking The Bags

The State Of Play Today

There are a few more interesting trends playing out right now, in the quick commerce landscape:

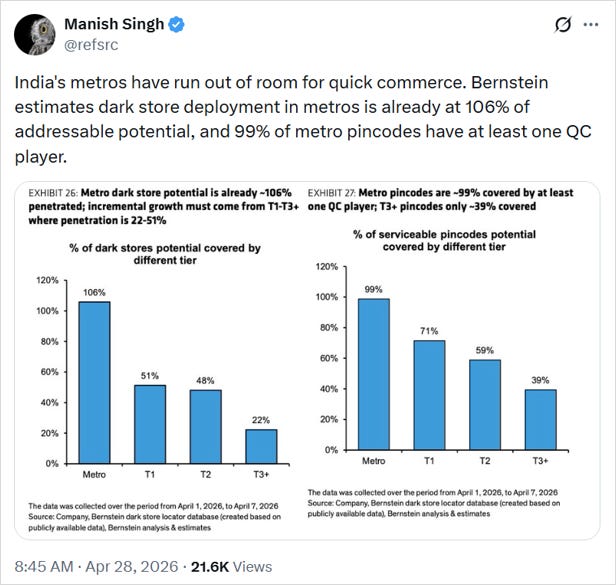

QC NOV is concentrated in the top 8 metros - and as per a recent Bernstein report, these metros are now saturated on dark store coverage; with 99% of their pin codes covered by at least 1 QC player, and over 80% of pin codes covered by 3 or more players. Manish Singh had shared a snapshot from this report:

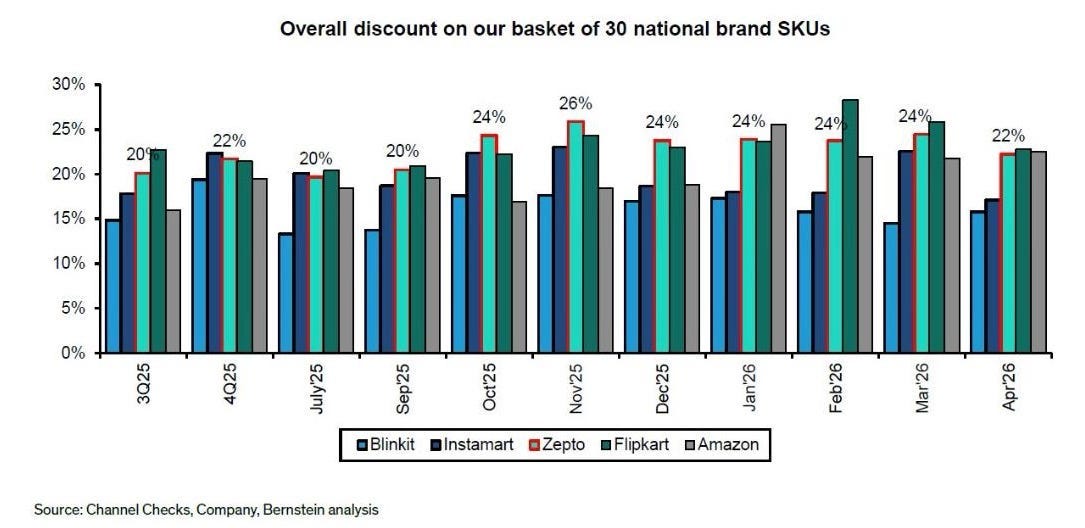

Yet at the same time, with Blinkit on track to reach 3000 dark stores by Mar’27, alongside Amazon Now and Flipkart Minutes driving aggressive expansion plans, we can expect another 1500 - 2000 dark stores to be added by the end of this year. Which means that the competition for affluent metro QC shoppers will only increase, and hence…

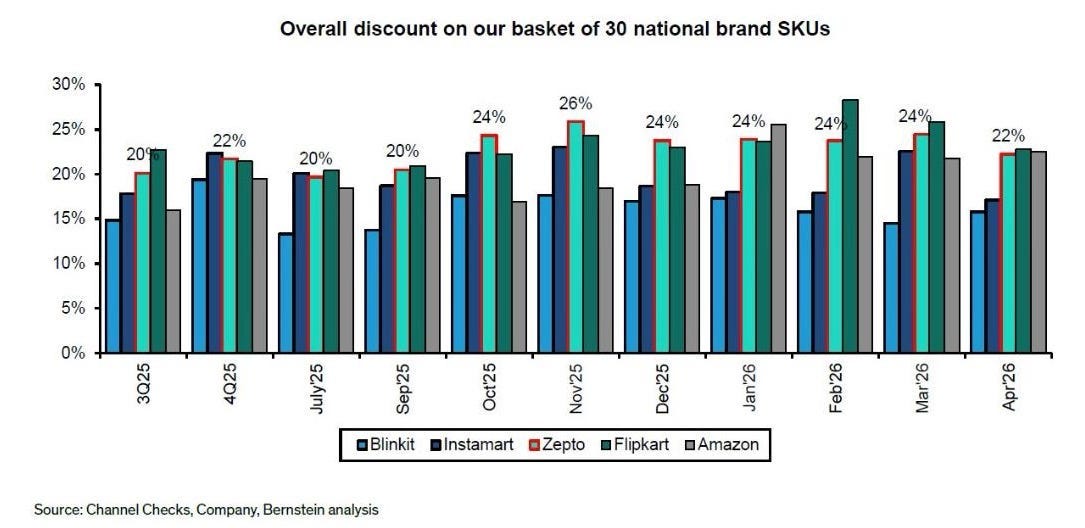

Amazon Now and Flipkart Minutes have ramped up discounts to acquire shoppers; while Zepto has maintained high discounts since Oct’25, in line with its strategy of being a value-led QC platform. Blinkit has held on its strategy of not playing primarily on pricing, while Instamart has reduced discounts from Dec’25 onwards, choosing to prioritise margins. Sanjeev Srivastav shared a graph illustrating this:

On the brand side as well, QC seems to be seeing intensifying competition, across multiple vectors:

Instamart’s Noice private label grew its SKUs from 200 in Aug’25 to 350 in Jan’26, and continues to enter new categories - most recently jumping onto the summer bandwagon with a range of ice-cream flavours.

New brands are continuing to enter QC at a rapid pace (search for any given category and scroll down a few pages to see what I mean). I remember being mildly surprised last year when Yellow Diamond chips started showing up on Instamart in Gurgaon; given that this brand was built on 5-rupee packs in GT. Seeing them drive sharing and party packs in an organized channel was definitely new.

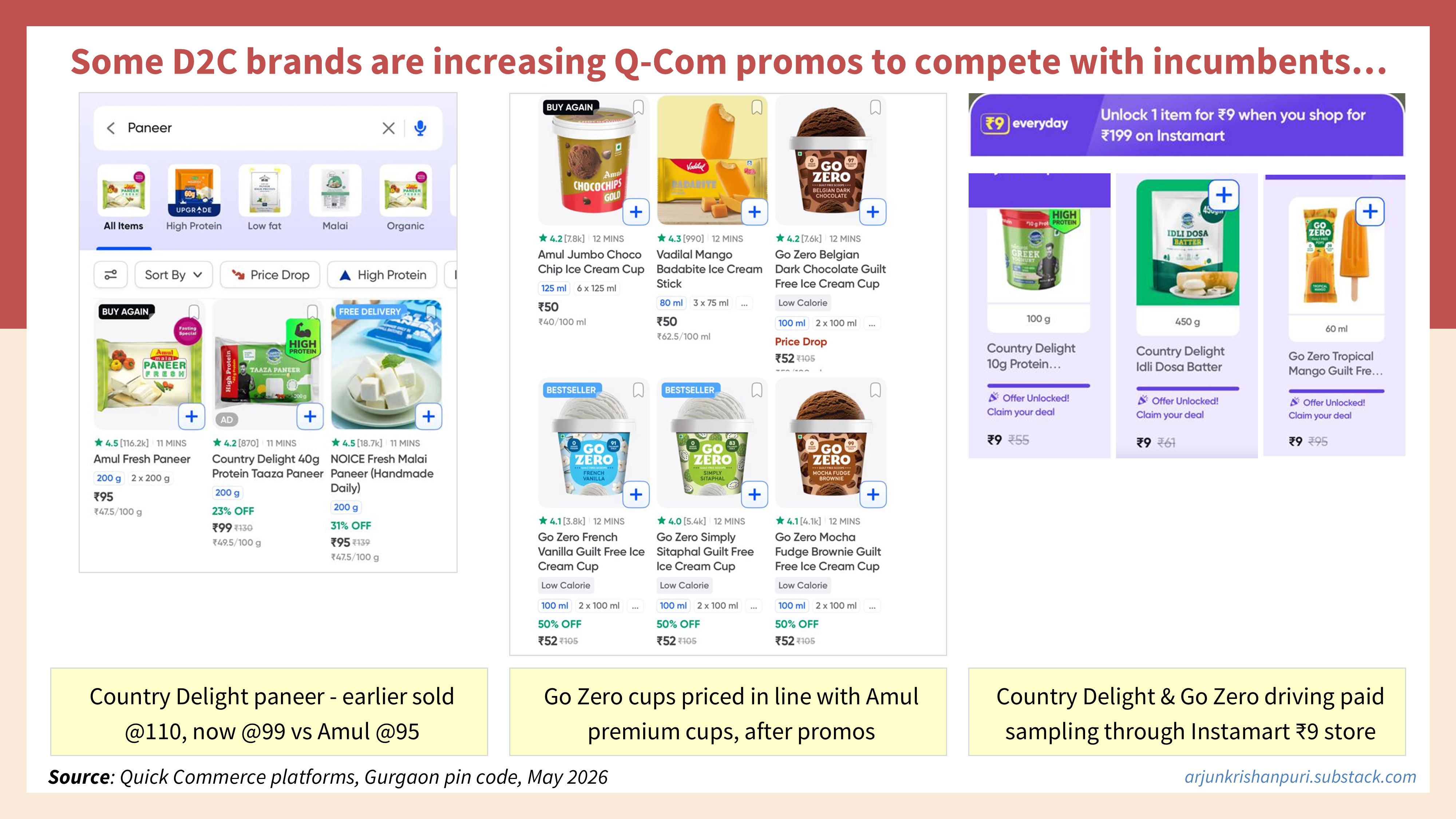

At least some insurgent consumer brands are increasing promos to compete with legacy brands - for example, over the past month, I’ve noticed Country Delight and Go Zero using paid sampling, and running higher discounts than in the past to compete with Amul:

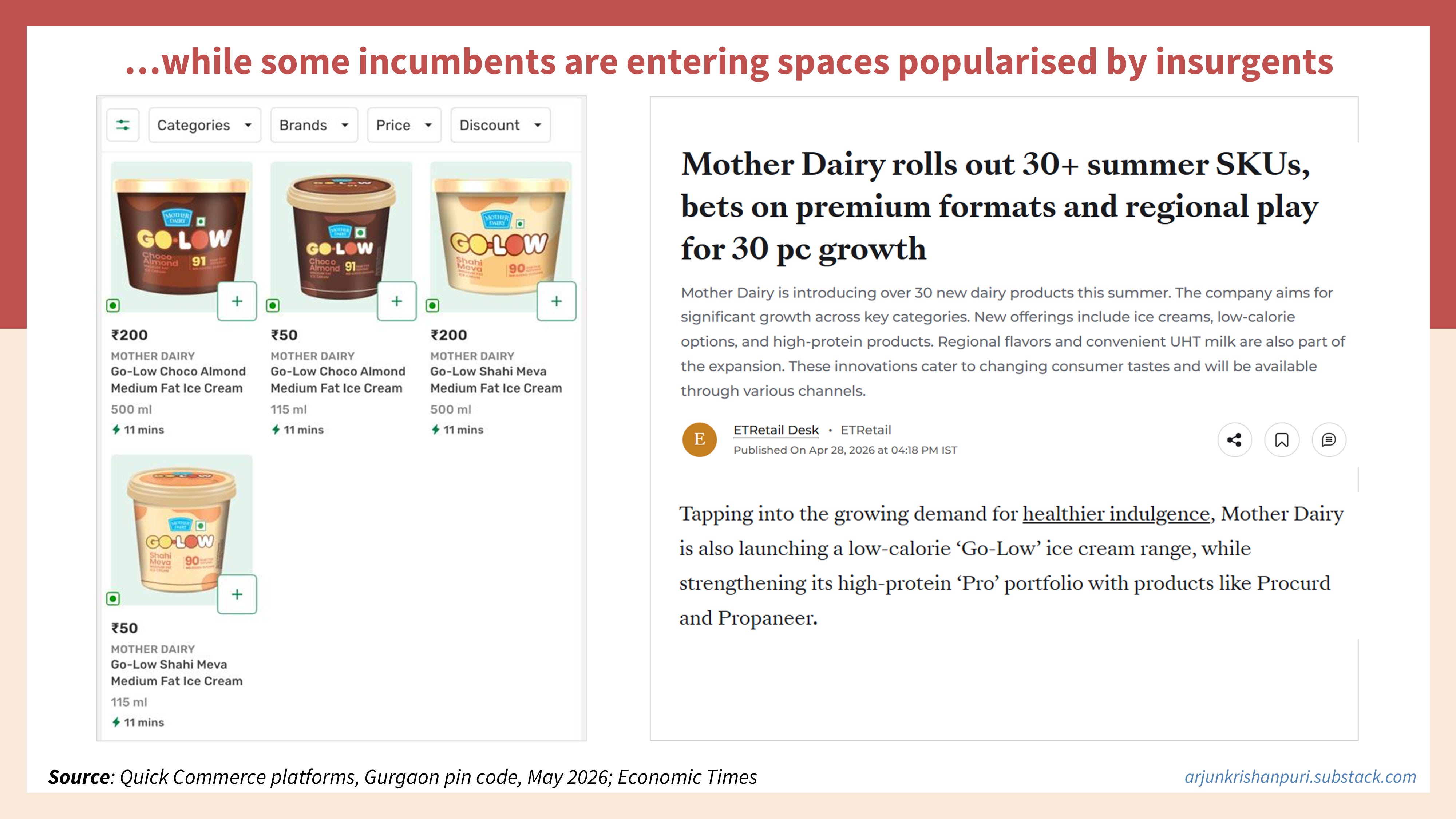

And interestingly, some legacy brands seem to be turning the tables by entering spaces recently popularised by insurgent brands - I was quite amused to see Mother Dairy’s new ‘Go Low’ brand of no-added-sugar ice cream (and they just launched high-protein curd and paneer, too).

The Post-Order Scratch Card

Where Do We Go From Here?

Quick Commerce is poised to remain the fastest-growing retail channel over the near-to-medium term.

However, new QC entrants are scaling up their dark store networks and increasing discounts at precisely the time when metro markets are approaching saturation (and the QC model in smaller cities is yet to be fully proven). Parallelly, brands on these platforms also seem to be competing more aggressively with each other than before.

Putting it all together - it looks like the the primary growth vector for QC platforms and brands is shifting from growth through channel & category expansion to growth through market share gains.

Over the past few years, quick commerce growth has been driven by expanding the market itself - opening dark stores, entering new markets, acquiring new shoppers, and adding categories.

Everything discussed above suggests that the next phase of growth may look different, though. If acquiring new-to-QC (or new-to-category) customers becomes harder going forward - then growth increasingly has to come from taking share from others.

On a related note, Swiggy CEO Sriharsha Majety made an interesting comment in a May’26 interview with the Economic Times:

“For us, it was a deliberate decision to assess what category growth could look like over the next three years and determine how long we could sustain elevated levels of negative unit economics. Given that the category growth over the last four to five quarters has been strong overall, we felt this was the right time to act, especially with newer entrants coming in, because last year’s growth is not guaranteed this year, and this year’s growth is not guaranteed next year.”

(emphasis mine)

If the first phase of Quick Commerce growth was a land grab, the next phase may be a battle royale.

I got the first call wrong by six months. The second one seems to have landed. I'll be back after Q2'26 results (and Zepto’s DRHP) are out, to see if this trajectory holds.